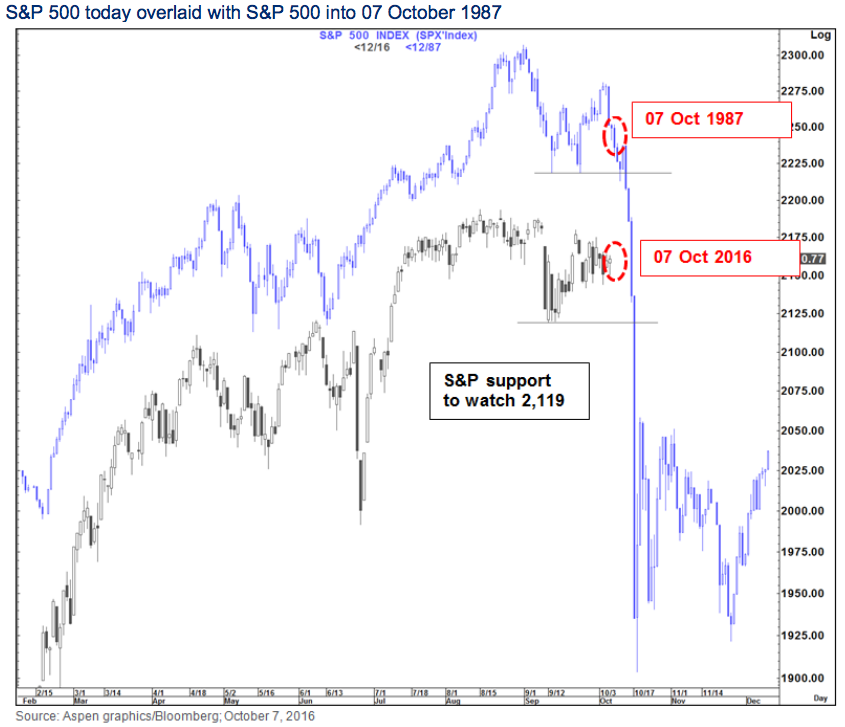

Although the seeds of the 2008 ‘financial crisis’ were sown at a much earlier period of time, the banking institutions continued to reap the benefits of ‘easy money’ until the financial crisis of 2008 negatively impacted the economy. The damage would have been much larger had U.S. taxpayer’s money not been used to bail out a large number of struggling banks and companies.

It is now more than eight years since the last financial ‘crisis’ has occurred and the current global situation is now beyond that of the financial ‘crisis’ of 2008. The Central Banks have been able to “kick the can down the road”, but that has only produced such vast proportions of debt that the next financial ‘crisis’ will not be manageable by the Global Central Banks.

European Banks have already begun the ‘crisis’:

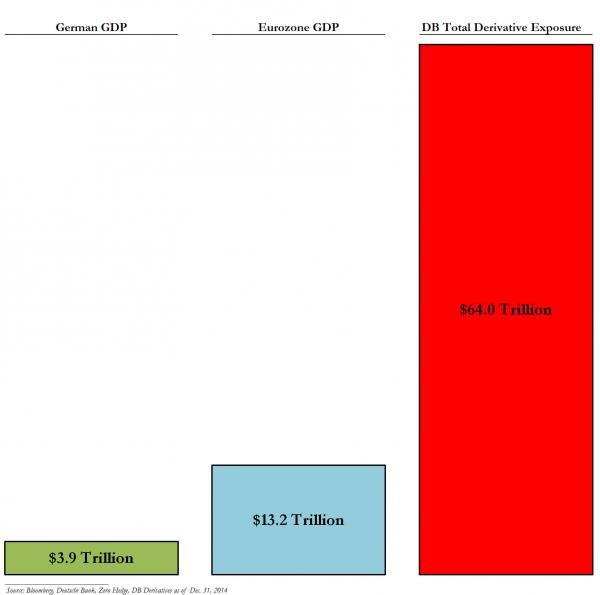

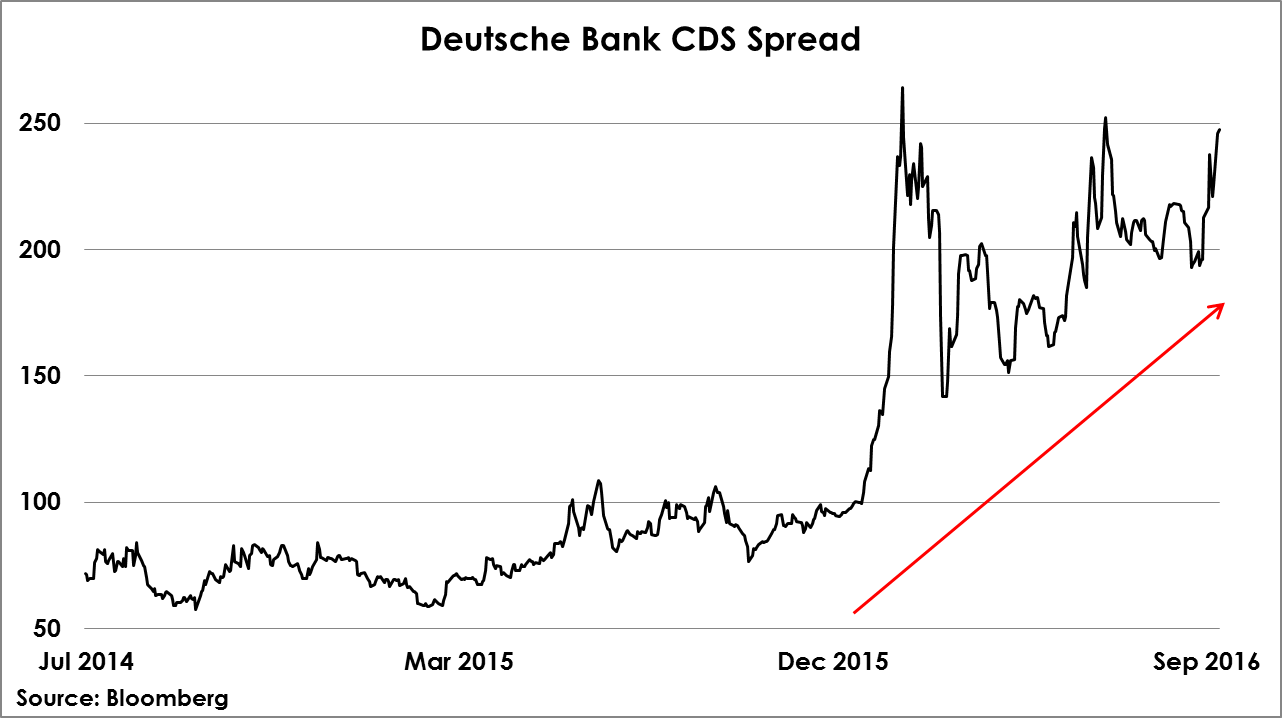

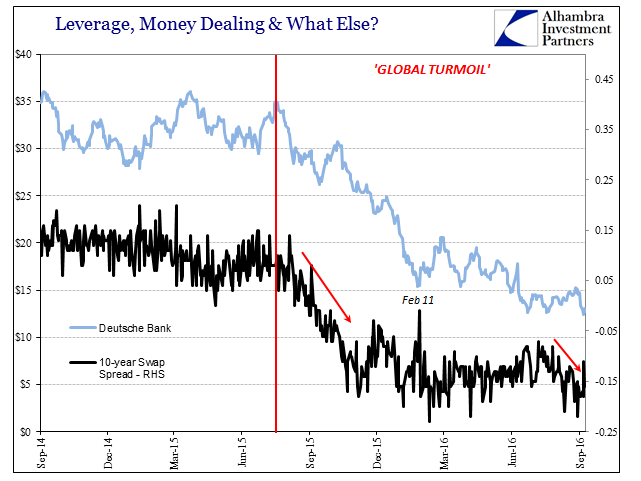

The world’s riskiest bank, according to the U.S. Federal Deposit Insurance Corporation, is the Deutsche Bank.

The Bank’s leverage ratio of 2.68% is far worse than that of what the U.S. banks were before the 2008 ‘crisis’.

“In 2008, the 10 largest US banks held on average 3.1% tangible equity capital-to-assets. When the financial crisis hit, these institutions experienced significant losses and required extraordinary government support,” said FDIC Vice Chairman Thomas M. Hoenig, reports the Business Insider.

The recent fine of $14 billion demanded as RMBS settlement, by the U.S. authorities, is 80% of the bank’s market cap and twice the amount that the bank has in reserve for litigations. The Deutsche Bank is on the brink of collapsing and will need a full-fledged bailout immediately.

However, it is not only the Deutsche Bank. There are other European banks in trouble, as well. Primarily, it is the Italian banks which are under considerable pressure.

With a GDP of approximately €16.2 trillion (nominal), the European Banks have approximately €1.2 trillion of bad loans. The total non-performing loans, of the Italian banks, is around €360 billion which represents 20% of Italy’s GDP.

However, Italian and German counterparts both continue to spar over their struggling banks.

Recently, the Italian Prime Minister Matteo Renzi told Bundesbank Chief Jens Weidmann to sort out the mess of the German banks which have “hundreds and hundreds and hundreds of billions of euros of derivatives”, rather than worry about the Italian banks.

“The European Banking Authority said in July that the region’s banks may need as much as 470 billion euros ($524 billion) in additional MREL-eligible funding. The EBA sample consisted of 114 banks representing 70 percent of the EU’s banking assets, including lenders not overseen by the SRB,” said Elke Koenig, Single Resolution Board Head, who is the resolution authority for 142 banks, reports Zero Hedge.

Will U.S. banks be immune to a financial ‘crisis’ since their European counterparts are experiencing such a ‘crisis’?

Although the Fed Chairwoman Janet Yellen wants us to believe that the large U.S. banks are in a much better situation as compared to 2008, because they “have put in place numerous steps and have more in the works that will strengthen these [financial] institutions, force them to hold a great deal of additional capital, and reduce their odds of failure. There will be much lower odds that a so-called systemic firm will fail, and should that occur, we’ll have better tools to deal with it”.

What is the reality? Even before the 2008 ‘crisis’, the regulators of Bear Stearns, Wachovia, Washington Mutual, Fannie Mae and Freddie Mac all kept on assuring the public that the institutions were well-capitalized, until the very end.

Therefore, we cannot accept the regulator’s word as final and/or factual truth.

In a recently published paper for the Brooking Institute, authors, former Treasury Secretary Larry Summers and Harvard Ph.D. candidate in economics, Natasha Sarin found the opposite to be true!

“To our surprise, we find that financial market information provides little support for the view that major institutions are significantly safer than they were before the crisis and some support for the notion that risks have actually increased,” the authors wrote.

The authors analyzed the six largest U.S. banks and fifty of the largest banks, around the world.

Conclusion:

Multiple experts like Steve Eisman have pointed out that the next financial ‘crisis’ will originate within the European Union. The politics of the region is unlikely to allow for a logical solution to the problems plaguing both the Italian and the German banks.

If one had believed the regulators, in 2007, they would have incurred huge losses. Similarly, if one believes that the American banks are immune to the next financial ‘crisis’, believe so at your own risk.

This is the beginning of “The Great Reset”, globally.

Learn more and profit from this big change in within the financial sector.

Chris Vermeulen – www.TheGoldAndOilGuy.com